The Map, Updated

A standalone analysis, written in mid-June 2026.

The map has not changed. The evidence for it arrived all at once, and most people are reading the evidence as the refutation.

In the past month, gold has fallen below a line it had held for over two years. Bitcoin has touched a level it reaches only at moments of maximum fear. The Federal Reserve has held rates and turned hawkish in the same breath. To the casual reader, each of these says the same comforting thing: the inflation story is over, the hard-money case has failed, the system is fine.

Read together, and read against the map, they say the opposite.

The map, put simply

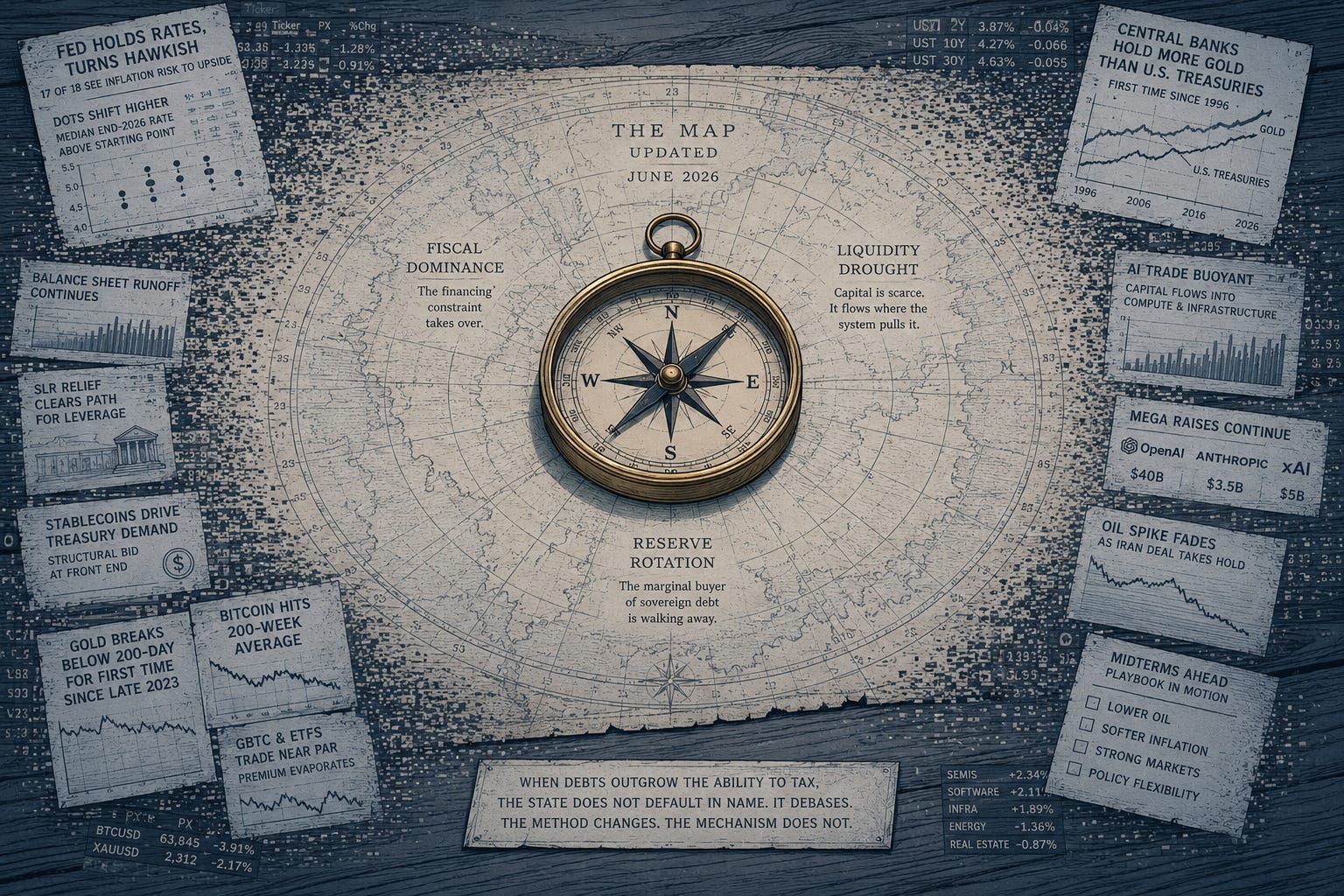

The map is a single claim, and it is older than any of us.

When a state’s debts grow faster than its ability to tax, and those debts can no longer be repaid in real terms, the state does not default in name. It debases. It allows inflation to do quietly what an open default would do loudly: reduce the real value of what it owes. Rome did it by shaving its coinage. Every paper-money empire since has done it by expanding the supply of the thing the debt is denominated in. The method changes. The mechanism does not.

The modern version has a clinical name that economists use without alarm. Fiscal dominance. It is the point at which monetary policy stops serving price stability and starts serving the financing of the deficit. The central bank does not announce the handover. It simply arrives at a place where it can no longer fight inflation, because fighting inflation would break the government’s ability to fund itself.

That is the whole map. Structural deficits, a debt load too large to grow out of, and a slow surrender of the printing press to the budget. The only question the map ever asked was whether this system would walk the same road as every heavily indebted state before it. The last month is that question being answered.

The items, and how each one updates the map

The evidence falls into three groups. Each one moves the map from theory toward confirmation.

The first group is the policy machinery, and it is where fiscal dominance becomes visible. In June the Federal Open Market Committee held rates unanimously and, in the same set of projections, flipped hawkish, with the median official now expecting rates to end the year higher than they began it and seventeen of eighteen judging the risk to inflation to be upward. Read plainly, that is a committee admitting the inflation it faces is not the kind its tool was built for. When price pressure comes from an energy shock and a structural deficit rather than from runaway private credit, raising the policy rate addresses the wrong variable. The hawkish dots are not confidence. They are the fiscal dominance question stated in the Fed’s own hand.

Beneath that sits the architecture being quietly assembled to finance the deficit without calling it what it is. Cut short rates, let the balance sheet run down to steepen the curve, and loosen the leverage rules so banks can absorb government debt with leverage. It is quantitative easing without the label, routed through the banking system rather than the central bank’s own book. The new Chair has been clear he prefers less forward guidance and fewer fixed signals, which is exactly the discretion such a manoeuvre requires. And in a smaller, stranger way, the dollar stablecoins now carry a standing, automatic bid for short-dated Treasuries, a structural change in who finances the government at the front end. The buyer of last resort is being rebuilt in several places at once.

The second group is the liquidity drought, and it is where the map shows up in prices. Gold has closed below its two-hundred-day moving average for the first time since late 2023. Bitcoin has fallen to its two-hundred-week moving average, the line it has only ever touched at cycle lows. The leveraged Bitcoin vehicles that once ran on a large premium to their holdings now trade close to parity, their flywheel stalled. The instinct is to read all of this as a verdict on the assets. The structural read is the reverse. Two of the hardest assets in the world are falling together, at the same time, while equities tied to artificial intelligence hold up and the most capital-hungry private names in the world raise enormous sums. That is not a story about gold or Bitcoin failing. It is a story about liquidity being scarce and being absorbed elsewhere, into the build-out of compute and the companies financing it.

The third group is the slowest and the most important. For the first time since 1996, the world’s central banks now hold more gold than they hold US Treasuries. The official sector, the most price-insensitive and longest-horizon buyer there is, has rotated out of sovereign debt and into a neutral asset with no issuer. This is not a trade. It moves in years. It is a quiet vote on the credibility of the dollar-Treasury system by the very institutions that built it, and it changes the assumptions underneath reserve-currency status itself.

Three groups, one direction. The financing constraint is taking over, the liquidity it consumes is draining the hardest assets, and the marginal buyer of government debt is walking away.

The midterms, the map, and the items

None of this happens in a vacuum. There is an election coming, and an administration that wants to hold control through it.

The setup is being built in plain sight, and it is the universal pre-election playbook rather than the property of any one party. A framework to end the conflict with Iran is being signed, and the oil price that spiked through the war is already unwinding, which should soften headline inflation into the autumn. The equity market is buoyant on the artificial-intelligence trade. A new Fed Chair has come through his first meeting reading as independent while assembling the structures, fewer signals and more discretion, that a future easing would need. And there is a foreign-policy result to point to. Lower inflation, rising markets, and a win abroad is the combination any incumbent would want walking into a midterm, and the strain of engineering it is being managed with some skill.

The other side of the ledger is the response to the same arithmetic. When a government cannot meet its obligations from the existing tax base, it reaches for what is mobile, new, and visible. Illinois has just signed a tax on digital-asset transactions that bites at the moment of transacting, including moving coins between a person’s own wallets, regardless of whether a profit was made. California has a billionaire wealth tax on the November ballot that counts digital assets in the total and is written to anchor residency early, so that capital cannot simply leave for Texas once it passes. At the federal level the revived Ultra-Millionaire Tax, the proposal associated with Senator Elizabeth Warren, adds an annual levy on large net worths and a forty per cent exit tax on those who renounce citizenship to escape it. The detail that matters is the exit tax. You only build a wall around capital that is already trying to leave.

Read structurally, both sides are symptoms of the same condition, and neither is the hero of this piece. One manages the optics of the cycle. The other reaches for new bases to tax. Both are what fiscal dominance looks like before it is named. And the younger reader, watching a hostility to the new ownership rails on one side, and a President willing to govern through division while the institutions that finance the state are reshaped on the other, draws the only conclusion available: the old order is closing the exits, whoever is holding the door.

The map is indifferent to who wins in the autumn. The financing constraint survives the result.

How the map develops from here

The direction of travel is not a forecast. It is the logic of the position.

The constraint tightens, and the policy response is the easing architecture already being built: lower short rates, a steeper curve, and banks levered into government debt to do the work the central bank no longer wants its own balance sheet to be seen doing. The obstacle right now is the shape of the curve. A flat curve removes the spread that makes banks willing to absorb that debt, which is why the curve, the term premium on the long bond, and the leverage rules are the things to watch, not the headline policy rate. The end of the war and a falling oil price may be exactly the cover an easing needs.

The tells to watch are the ones already moving. If gold and Bitcoin are functioning as liquidity gauges in this regime rather than as inflation hedges, then their weakness is a reading of the drought, and the historical sequel to a drought of this kind is an injection. The pattern in gold has rhymed before: a breakdown, then a policy response, then a recovery. Whether it rhymes again is the open question. The mechanism says watch the plumbing, not the narrative.

Takeaways

The map did not change this month. The evidence for it arrived, and arrived disguised as its refutation.

A hawkish Fed holding into structural, energy-driven inflation is fiscal dominance stated out loud.

Gold and Bitcoin falling together is a liquidity signal, not a verdict on either asset.

Central banks holding more gold than Treasuries is the marginal buyer of government debt quietly stepping back.

The election will be fought over the symptoms. The condition is not on the ballot.

The structure the mainstream miss

Read one at a time, each item is both bearish and reassuring. Gold down means the inflation hedge has failed. Bitcoin down means the thesis is broken. A hawkish Fed means inflation has been beaten. A new tax means the state is getting its house in order.

Read as one system, they are the same event. A heavily indebted state is entering fiscal dominance. The liquidity that would ordinarily support the hardest assets is being drained into the financing of the deficit and the build-out of artificial intelligence. The price signals of those hard assets are being suppressed by the very drought the map predicts. And the largest, slowest buyers of government debt are rotating into the one asset the state cannot print.

The single thing the mainstream miss is this. In a regime of fiscal dominance, weakness in the hardest assets is information about liquidity and market structure, not about their monetary case. It is a falsifiable claim, and it is the opposite of the comfortable one.

Final thought

The map was never a prediction. It is a description of the road every heavily indebted state has eventually walked, and the only thing left unknown was whether this one would walk it too.

The last month is the answer, arriving all at once, wearing the face of its opposite.